In today’s financial world, payment modernization is no longer a luxury, but a necessity.

European banks are facing a unique challenge.

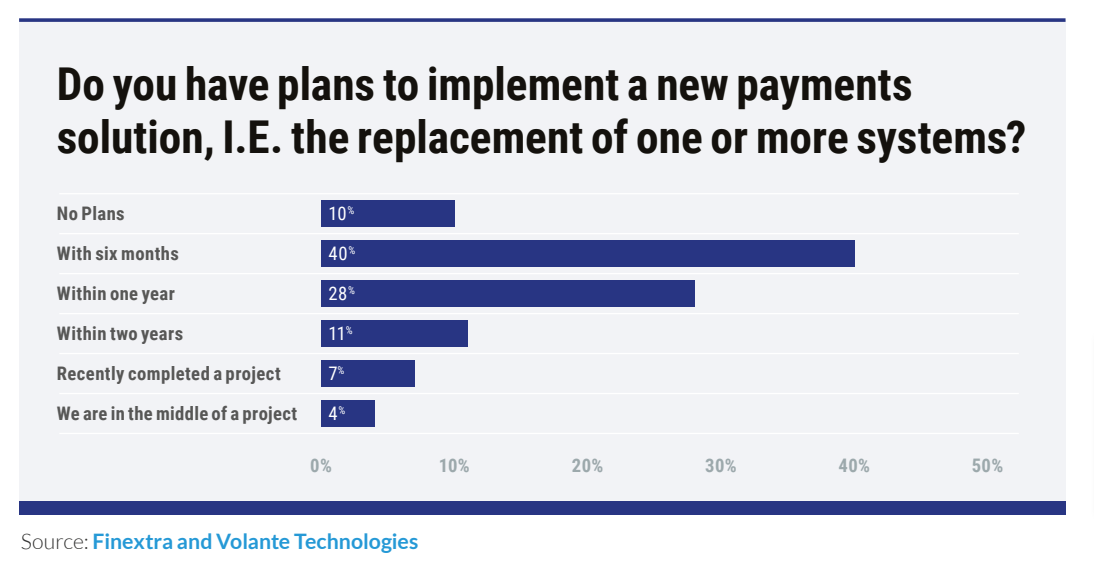

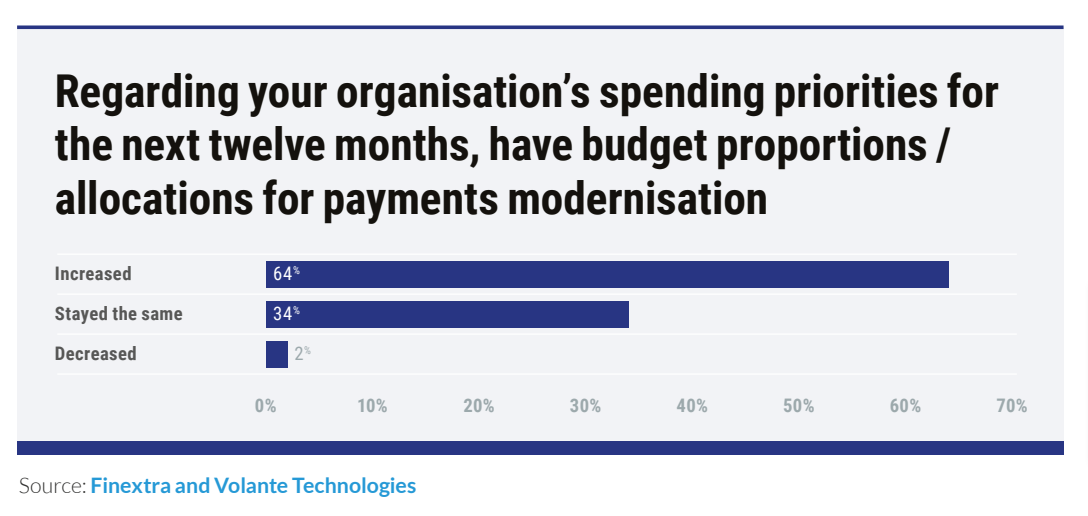

A recent study by Finextra and Volante Technology sheds light on the significant stakes for banks to modernize in order to remain competitive.

They are at the forefront of open banking and API initiatives, while navigating a complex environment of real-time and cross-border payments.

The year 2023 marks a turning point with the changes in the SEPA regulations by the European Payments Council (EPC), pushing banks of all sizes towards the ISO 20022 standard.

This transition is not trivial. It represents a major challenge for banks in the next 12 months.

Thus, modernizing legacy systems becomes imperative in this rapidly evolving digital context.

A survey by Finextra and Volante reveals that 67% of financial institutions are seeking new payment modernization products in the coming year.

The main pain point for 79% of the global banks surveyed is access to real-time payments and real-time liquidity.

The cost of maintaining and upgrading these systems is also prohibitive.

75% of respondents emphasize the cost of payment processing as a key driver.

These factors trigger a fundamental shift in the demand for payment modernization in the market, leading to an increased adoption of Payments-as-a-Service (PaaS) globally.

In this context, European banks must rethink their systems to remain competitive and resilient.

1. Why Modernize?

Payment modernization is essential for banks looking to secure and expand their market share.

It is synonymous with innovation and competitiveness in a constantly evolving sector.

At the heart of this transformation, the customer experience must be seamless and frictionless, regardless of the payment channel used.

Adopting ISO 20022 standards goes beyond mere compliance.

It offers banks the opportunity to leverage rich data to optimize their operations and seize new growth opportunities.

Modernization is not just a response to current regulatory requirements.

It prepares banks to quickly adapt to future changes in the regulatory landscape.

By embracing modernization, banks position themselves as innovators and leaders in the industry.

It also allows them to use data as a versatile tool for cross-selling across different business verticals.

In a rapidly changing financial landscape, adopting these transformation strategies becomes imperative for banks eager to maintain their competitive edge and support their growth.

2. European Challenges and Deadlines

European banks are faced with key regulatory deadlines that shape their payment modernization journey.

The year 2023 is particularly crucial with the introduction of major changes in the EPC’s SEPA regulations.

These changes compel banks to adopt the ISO 20022 standard, a global benchmark for financial message exchanges.

This transition is not straightforward. It represents a significant challenge, especially for banks still managing legacy systems.

These older systems are often rigid and unsuited to the demands of modern payments.

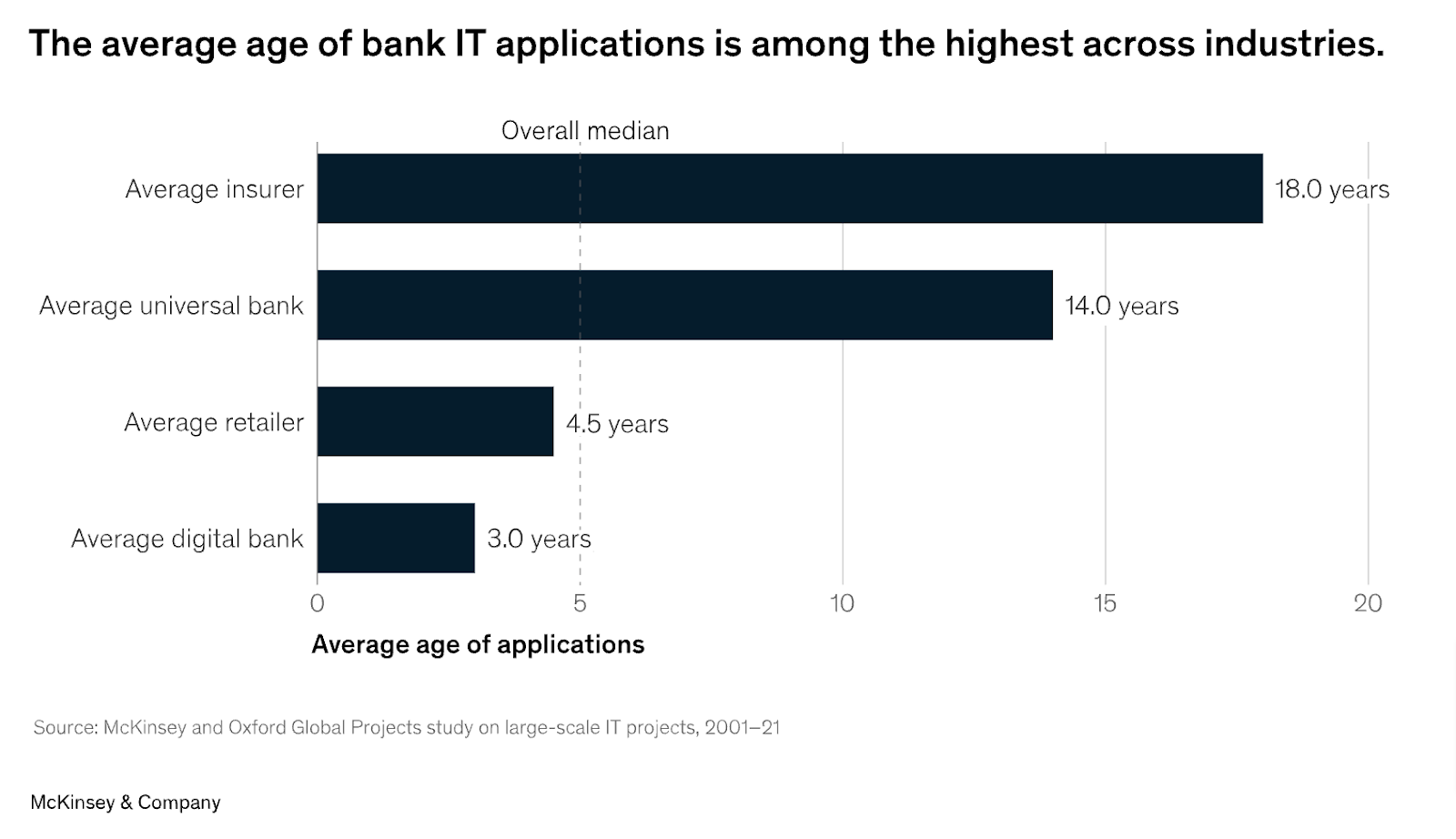

According to McKinsey research, the average age of IT applications in universal banks is 14 years, significantly more than the 3 years in digital banks.

This disparity underscores the urgency of modernization to remain competitive.

Banks must not only meet these regulatory requirements but also prepare for future developments.

The ability to rapidly adapt to these changes is now a key element of survival and success in the banking sector.

Faced with these challenges, European banks must act swiftly to modernize their payment systems, while keeping an eye on upcoming regulatory and technological advancements.

FOCUS: Adoption of ISO 20022 Standard and Details on HVPS+ and CBPR+

The year 2023 is marked by the mandatory adoption of the ISO 20022 standard by European banks, a change that profoundly affects High-Value Payment Systems (HVPS) and Cross-Border Payments (CBPR).

HVPS+ (High-Value Payment Systems Plus):

Definition: HVPS+ refers to the enhanced version of high-value payment systems, adapted to the ISO 20022 standard.

Impact on High-Value Transactions: With the introduction of HVPS+, high-value transactions benefit from greater data richness and improved traceability. This allows for more in-depth transaction analysis and better risk management.

Improvement in Interoperability: HVPS+ enhances interoperability among various global payment infrastructures, thereby facilitating high-value cross-border transactions.

Implementation Challenges: Implementing HVPS+ requires a significant overhaul of existing systems, which can be a challenge for banks with legacy infrastructures.

CBPR+ (Cross-Border Payments and Reporting Plus):

Definition: CBPR+ is the adaptation of cross-border payments and reporting to the ISO 20022 standard.

Improvement in Cross-Border Payments: CBPR+ aims to standardize and simplify cross-border payments, offering better data quality and increased efficiency.

Reduction in Fees and Delays: With CBPR+, banks can reduce the fees and delays associated with cross-border payments, thus improving the customer experience.

Compliance Challenges: Compliance with CBPR+ involves navigating a complex regulatory environment, particularly concerning different jurisdictions and regulations.

The adoption of the ISO 20022 standard and the implementation of HVPS+ and CBPR+ represent crucial steps for European banks.

These changes offer significant opportunities to enhance the efficiency of high-value and cross-border payments, while also presenting challenges in terms of system upgrades and regulatory compliance.

For banks, successfully navigating this transition is essential to remain competitive in the evolving global financial landscape.

3. The Impact of Payments-as-a-Service (PaaS)

Payments-as-a-Service (PaaS) emerges as a key catalyst in the modernization of payments for European banks.

This approach provides a flexible and scalable alternative to traditional payment systems.

With PaaS, banks can outsource their payment infrastructure, which reduces operational costs and accelerates innovation.

The adoption of PaaS is on the rise, a trend driven by the need to quickly respond to market changes and regulatory requirements.

PaaS enables banks to focus on their core business while benefiting from the latest payment technologies.

It also offers greater agility in integrating new services and meeting the changing expectations of customers.

Furthermore, PaaS facilitates access to real-time payments, an increasingly crucial element in the current financial ecosystem.

For European banks, investing in PaaS means staying at the forefront of innovation, while effectively managing costs and enhancing the customer experience.

4. Bank Strategies and Key Factors for Their Future

European banks must consider several key factors in their payment modernization journey.

The first step involves assessing and updating existing infrastructure.

It is crucial to replace or modernize legacy systems to ensure operational flexibility and efficiency.

Understanding and adopting ISO 20022 standards is also crucial.

These standards provide opportunities for streamlining and optimizing processes.

Banks must also stay alert to regulatory and technological developments.

This requires constant vigilance and the ability to quickly adapt to new requirements.

Focusing on innovation and improving customer experience is another key factor.

Banks need to explore new technologies, such as artificial intelligence and blockchain, to enhance their payment services.

Finally, collaborating with technology partners, especially through PaaS, can offer significant benefits in terms of efficiency and innovation.

By considering these factors, European banks can not only meet current challenges but also position themselves for future success in the evolving financial landscape.